You bought Bitcoin in 2021, maybe some Ethereum later, and now you’re sitting on gains. But if you live in or earn income from Mexico, those digital coins aren’t just numbers on a screen-they’re taxable assets. The confusion around crypto taxation in Mexico is real because the government hasn’t written a specific law for it. Instead, they treat your crypto like any other piece of property.

This means your taxes depend on how you use that crypto, who you are (individual or company), and when you sell it. Get this wrong, and you could face penalties from the Servicio de Administración Tributaria (SAT). Get it right, and you stay compliant while keeping more of your profits. Let’s break down exactly how the Mexican tax system handles your digital wallet.

How Mexico Classifies Cryptocurrency

Before we talk about rates, we need to understand what the Mexican government thinks your Bitcoin actually is. Under the Federal Civil Code, specifically Articles 758 and 763, cryptocurrencies are classified as intangible movable assets. This is a crucial distinction.

This classification means two things:

- It is not legal tender: You cannot force someone to accept Bitcoin as payment for debts or taxes in pesos.

- It is property: It is treated similarly to stocks, bonds, or even physical goods like furniture or cars for tax purposes.

Because it is property, the existing Value-Added Tax (VAT) and Income Tax (ISR) frameworks apply. There is no separate "crypto tax" department. Your crypto transactions fall under the general rules for buying and selling assets. This creates a realization-based system. You don’t pay tax just because the price of Bitcoin went up. You only pay tax when you actually sell, trade, or spend it.

Tax Rates for Individuals vs. Companies

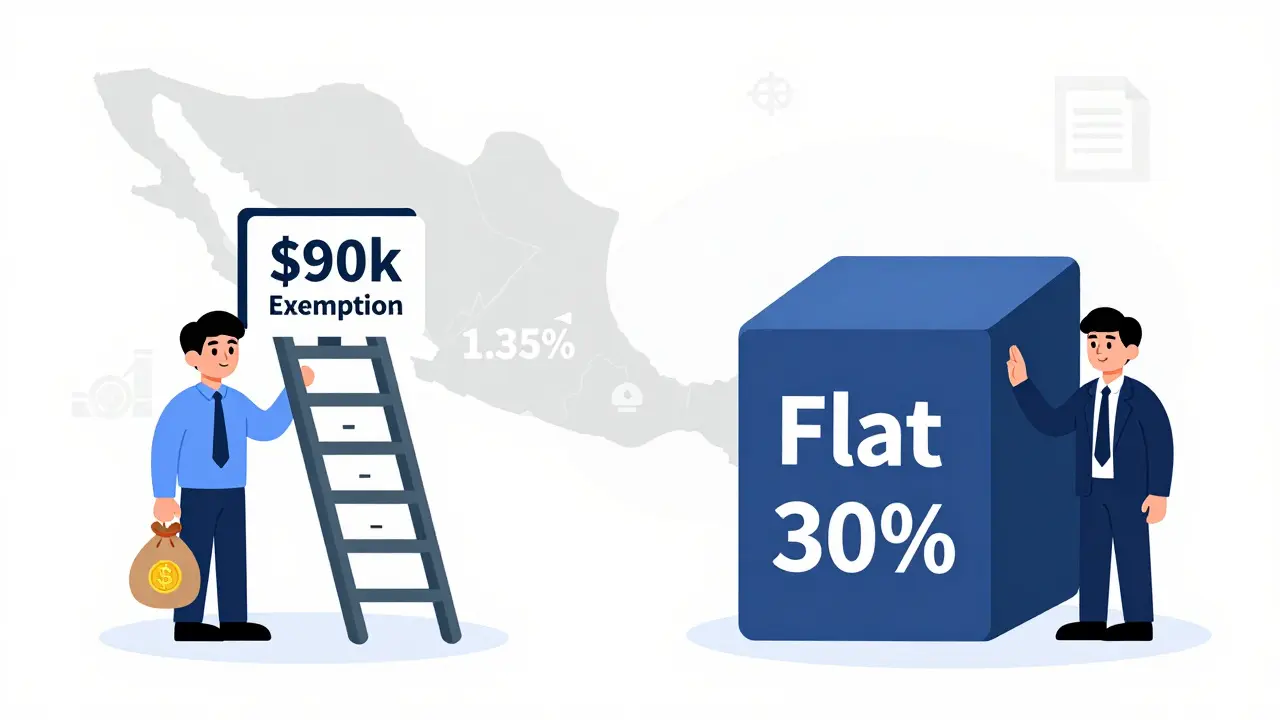

The amount you owe depends entirely on whether you are filing as an individual person or as a legal entity (like an S.A. or S.R.L.). The Mexican Income Tax Law does not distinguish between "ordinary income" and "capital gains" for individuals, which can be surprising if you are used to systems like the US where long-term holdings get lower rates.

| Taxpayer Type | Tax Rate Structure | Key Details |

|---|---|---|

| Individuals | Progressive (1.92% - 35%) | Based on total annual income. Includes all sources, not just crypto. |

| Corporations/Legal Entities | Flat 30% | Applies to all net profits from crypto trading or services. |

For Individuals

If you are a Mexican resident individual, your crypto gains are added to your other income (salary, freelance work, etc.) and taxed at your marginal rate. The current progressive scale ranges from roughly 1.92% for very low incomes up to 35% for high earners. Here is the good news: there is an annual exemption. Individuals benefit from a tax-free allowance on capital gains from the sale of movable property. This threshold is approximately $90,000 Mexican pesos (roughly USD $4,000-$5,000 depending on exchange rates). If your total crypto gains for the year stay below this amount, you may not owe any income tax on them. However, once you cross that line, the entire gain is subject to your progressive tax bracket.

For Corporations

If you operate through a company, the math is simpler but potentially higher. Corporate income tax on cryptocurrency gains is levied at a flat rate of 30%. This applies regardless of how long you held the asset. Whether you day-trade or hold for five years, the profit is taxed at 30% after deducting allowable business expenses.

When Do You Actually Owe Tax? (Realization Events)

This is where most people make mistakes. In Mexico, holding crypto that increases in value is not a taxable event. You do not report unrealized gains. You only trigger a tax liability when you dispose of the asset. Here are the common scenarios:

- Selling for Fiat: Converting Bitcoin to Mexican Pesos (MXN) or US Dollars (USD) is a clear sale. You calculate the difference between your purchase price (cost basis) and the sale price.

- Crypto-to-Crypto Trades: Swapping Bitcoin for Ethereum is treated as two events: selling the Bitcoin and buying the Ethereum. You must recognize a gain or loss on the Bitcoin portion based on its fair market value at the time of the swap.

- Spending Crypto: Using crypto to buy goods or services (even a coffee) is considered a disposition. You are effectively selling the crypto to pay for the item. The value of the crypto at the moment of purchase determines your cost basis for that transaction.

- Receiving Payment: If you are paid in crypto for freelance work, that is ordinary income. You must declare the peso equivalent of the crypto received as part of your professional earnings.

Note that mining income is generally treated as ordinary income at the fair market value when the coins are received, not when they are later sold. Subsequent sales then trigger capital gains calculations based on that initial income value.

Value-Added Tax (VAT) Considerations

Beyond income tax, you need to consider VAT. Since cryptocurrencies are intangible assets, transactions involving them can be subject to the standard VAT rate in Mexico, which is currently 16%. However, the application here is nuanced.

For pure peer-to-peer transfers between individuals, VAT often doesn't apply directly to the transfer itself. However, if you are a business providing crypto-related services (such as an exchange, a broker, or a consulting firm), those services are generally subject to VAT. Additionally, if you use crypto to purchase taxable goods or services, the vendor will charge VAT on the transaction as normal. The key takeaway is that while the *gain* is taxed via ISR, the *activity* of facilitating crypto trades may incur VAT obligations for businesses.

Compliance and Reporting Requirements

Taxes are only half the battle. Mexico has strict anti-money laundering (AML) regulations that intersect with crypto usage. The regulatory landscape involves multiple bodies, including Banco de México, the Ministry of Finance, and the National Banking and Securities Commission.

Even if you are not a licensed financial institution, you must be aware of reporting thresholds. Transactions involving virtual assets conducted by non-financial entities are classified as "vulnerable activities." These must be reported to the Ministry of Finance if the amount equals or exceeds approximately USD $3,500 (or the peso equivalent). This is significantly lower than thresholds in many other countries, meaning frequent traders or large holders will hit this limit quickly.

Financial institutions, such as banks and registered fintechs, face even stricter rules. They require prior authorization from Banco de México to handle virtual assets and are prohibited from offering these services directly to the public without adhering to rigorous KYC (Know Your Customer) protocols. For the average user, this means using regulated exchanges that already handle much of this reporting, but you remain responsible for your own tax filings.

Record Keeping: Your Best Defense

Because there is no single automated system that tracks your crypto across different wallets and exchanges, the burden of proof is on you. The SAT requires detailed records for all acquisitions and dispositions. You should maintain a ledger that includes:

- Date of Acquisition: When you bought or mined the asset.

- Cost Basis: How much you paid in MXN (converted at the exchange rate on that date).

- Date of Disposition: When you sold, traded, or spent it.

- Fair Market Value: The peso value of the crypto at the exact time of the transaction.

- Counterparty Information: Who you traded with, if applicable.

The general principle for calculating cost basis in Mexico follows the First-In-First-Out (FIFO) method unless you can prove otherwise. This means the first coins you bought are the first ones considered sold when you make a trade. Given the volatility of crypto, converting every transaction to pesos at daily exchange rates adds complexity, so using specialized tax software or hiring a local accountant familiar with digital assets is highly recommended.

Current Political Landscape and Future Outlook

As of mid-2026, under President Claudia Sheinbaum, the political stance on cryptocurrency remains cautious. The ruling Morena Party has not introduced a comprehensive crypto-specific tax code. Instead, they rely on amendments to existing laws. Some reports suggest a 20% tax on certain crypto gains has been discussed or implemented through broader legislative tweaks, but the core framework remains the general ISR and VAT laws described above.

There is little indication of a shift toward pro-crypto policies like those seen in El Salvador or Argentina. The focus remains on preventing illicit finance and ensuring tax collection. This means the status quo-treating crypto as intangible property-is likely to persist for the foreseeable future. Investors should plan for continuity rather than expecting new exemptions or favorable regimes.

Is Bitcoin legal in Mexico?

Yes, Bitcoin and other cryptocurrencies are legal to own and trade in Mexico. However, they are not recognized as legal tender. You cannot use them to pay taxes or settle debts unless both parties agree, and they are treated as intangible movable assets for tax purposes.

Do I have to pay tax if I just hold crypto?

No. Mexico uses a realization-based system. You do not pay income tax on unrealized gains. You only owe tax when you sell, trade, or spend your cryptocurrency, triggering a taxable event.

What is the tax-free limit for individuals?

Individuals benefit from an annual exemption on capital gains from movable property up to approximately $90,000 Mexican pesos (around USD $4,000-$5,000). Gains below this threshold may not be subject to income tax, but you must still track them accurately.

How are crypto-to-crypto swaps taxed?

Swapping one cryptocurrency for another (e.g., BTC for ETH) is a taxable event. It is treated as selling the first coin and buying the second. You must calculate the gain or loss based on the fair market value of the first coin at the time of the swap.

Are foreign residents taxed on crypto in Mexico?

Generally, non-Mexican residents are not subject to Mexican income tax on cryptocurrency transactions, even if they involve a Mexican counterparty, unless they have a permanent establishment or specific tax residency ties in Mexico. Consult a local tax advisor for complex cross-border situations.